13 Leading U.S. Semiconductor Companies in 2026

The United States dominates the global semiconductor ecosystem, not merely by chip output but by controlling the most critical components of the supply chain. From pioneering chip architectures to cutting‑edge software tools and high‑performance computing, U.S. firms generate over $500 billion in annual revenue—more than half of worldwide semiconductor earnings.

This guide breaks down the 13 most influential U.S. semiconductor companies, detailing their business models, flagship technologies, market positions, and key performance metrics. Whether powering AI, consumer electronics, or the next wave of computing, these firms are shaping the industry’s future.

Did you know? The CHIPS and Science Act of 2022 allocates $52.7 billion to strengthen U.S. semiconductor manufacturing and research—$39 billion for fabs and $11 billion for R&D and workforce development. [1]

13. NXP Semiconductors: Automotive Chip Leader

Founded 2006

Core Products: ADAS, RF, wireless communication solutions

Annual Revenue: $12.61 billion

Competitive Edge: NFC & embedded security chips

Originating from a Philips spin‑off, NXP excels in automotive, industrial, and secure connectivity solutions. Its chips are integral to ADAS, infotainment, powertrain control, and vehicle networking, while NFC technology powers contactless payments and IoT devices.

Key Insight: In 2026, NXP launched the S32N7 super‑integration processor to accelerate vehicle digitalization.

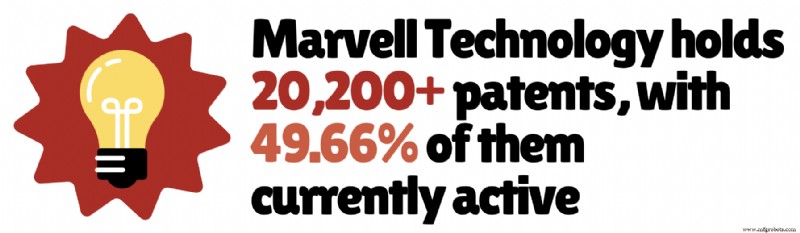

12. Marvell Technology: Data Infrastructure Innovator

Founded 1995

Core Products: ASICs, networking chips, storage controllers

Annual Revenue: $8.19 billion+

Competitive Edge: Leadership in custom AI silicon

Marvell drives data infrastructure and connectivity—enabling efficient data movement, storage, and processing in cloud, 5G, and AI workloads. Its chips underpin major cloud providers and hyperscale data centers.

Investing in 800 G and 1.6 T optical networking and AI cluster interconnects, Marvell’s AI demand has become its primary growth engine.

Key Insight: FY 2026 revenue reached $8.19 billion, propelled by AI‑centric demand. [2]

11. Analog Devices: Signal Processing Specialist

Founded 1965

Core Products: Analog ICs, mixed‑signal semiconductors

Annual Revenue: $11 billion+

Competitive Edge: Industrial & automotive focus

Analog Devices translates real‑world signals into digital data, making its chips indispensable for precision, low‑power applications across industrial, automotive, communications, and healthcare markets.

Its resilient business model—long product lifecycles and recurring demand—keeps revenue stable in cyclical markets.

Electrification, AI‑enabled infrastructure, and renewable energy are driving growth.

Key Insight: 45% of revenue comes from industrial, 30% from automotive, and 13% each from consumer and communications. [4]

10. KLA Corporation: Quality Control Authority of Chips

Founded 1975

Core Products: Wafer inspection, metrology tools

Annual Revenue: $13 billion+

Competitive Edge: Dominance in process control & inspection

KLA delivers precision inspection and metrology systems that ensure defect‑free chips. Advanced optics, AI algorithms, and high‑precision metrology detect near‑atomic‑scale defects critical for complex nodes.

With rising process complexity, KLA’s systems become even more essential, driving yield optimization and high manufacturing investment.

Key Insight: Revenue streams include service contracts, software upgrades, and data analytics, ensuring resilient cash flow even during downturns.

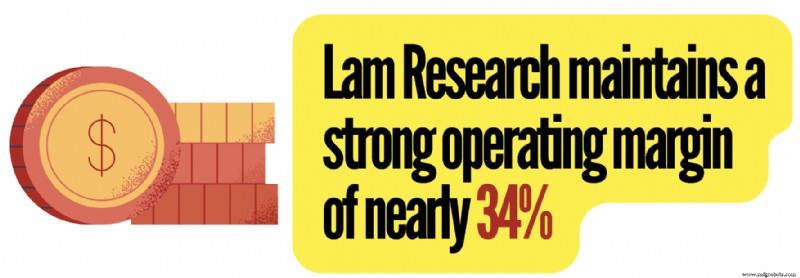

9. Lam Research: Precision Fabrication Specialist

Founded 1980

Core Products: Etching systems, deposition equipment

Annual Revenue: $21.6 billion+

Competitive Edge: Dominance in plasma etching

Lam Research supplies etching, deposition, and wafer cleaning technologies essential for building ultra‑small transistors. As nodes shrink below 5 nm, precision demands grow, driving higher demand for Lam’s advanced systems.

Key Insight: Its systems are also crucial for 3D NAND memory, supporting over 200 stacked layers.

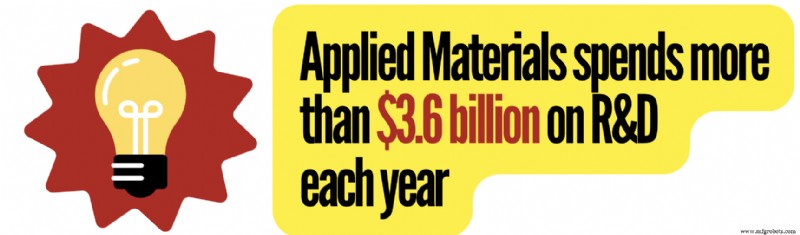

8. Applied Materials: Engine Behind Chip Manufacturing

Founded 1967

Core Products: Semiconductor manufacturing tools, deposition systems

Annual Revenue: $28.3 billion+

Competitive Edge: High switching costs

Applied Materials builds the advanced equipment that powers fabs worldwide—depicting the tools that enable the entire chip production chain.

Financially, it reports $28.36 billion in revenue and $7.83 billion in net profit, with a 49% gross margin reflecting the high value of its specialized tools.

Key Insight: Investing heavily in gate‑all‑around transistors and advanced DRAM scaling, Applied holds 57,700 patents, 45% of which remain active. [6]

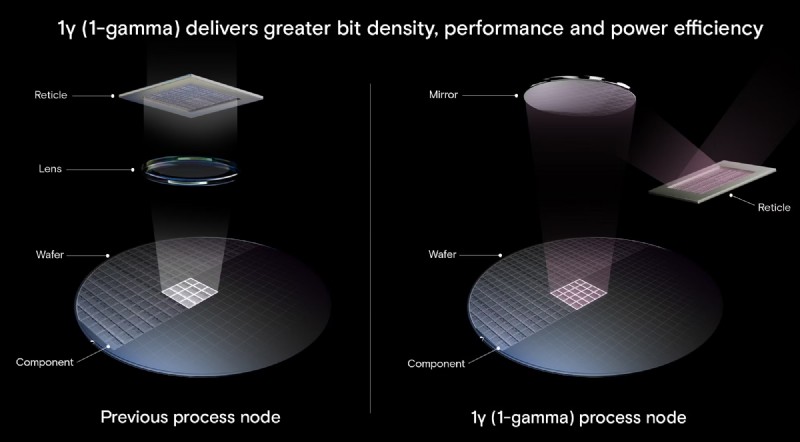

7. Micron Technology: The Memory Engine

Founded 1978

Core Products: DRAM, NAND flash, high‑bandwidth memory

Annual Revenue: $37.3 billion+

Competitive Edge: Long‑term supply contracts

Micron is the only major U.S. manufacturer of DRAM and NAND memory. AI workloads have turned memory from a commodity into a strategic driver, boosting demand for high‑bandwidth memory and large‑capacity DRAM.

Micron’s 1‑gamma DRAM and 200‑layer 3D NAND are at the forefront of this surge.

Key Insight: 77% of revenue stems from DRAM, 23% from NAND flash. [7]

6. Texas Instruments: Quiet Leader of Everyday Electronics

Founded 1930 (as Geophysical Service)

Core Products: Analog ICs, embedded processors

Annual Revenue: $17.6 billion+

Competitive Edge: Dominance in analog semiconductors

TI’s analog segment, valued over $110 billion, is expected to grow at ~6% CAGR through 2034. It supplies tens of billions of devices—smartphones, power systems, cars, industrial robots—making it the backbone of modern electronics.

Long product lifecycles (10–20+ years) yield predictable, stable revenue streams.

Key Insight: Gross margin approaches 58%, with analog sales constituting over 80% of total revenue.

5. Advanced Micro Devices: Redefining High‑Performance Computing

Founded 1969

Core Products: Ryzen, EPYC, Radeon, Instinct AI accelerators

Annual Revenue: $37.47 billion+

Competitive Edge: Data‑center growth with EPYC CPUs

AMD has risen from underdog to a major player across CPUs, GPUs, and AI accelerators. Its EPYC server CPUs and Instinct GPUs are key to AI and data‑center workloads.

Key Insight: FY 2026 data‑center segment grew 57% YoY, driven by EPYC and Instinct demand. [9]

4. Qualcomm: King of Wireless Connectivity

Founded 1985

Core Products: Snapdragon SoCs, 5G modems, RF systems

Annual Revenue: $44.4 billion+

Competitive Edge: Unmatched wireless patent portfolio

Qualcomm powers the global smartphone ecosystem with Snapdragon processors, commanding ~25% of SoC shipments and >70% in high‑end Android markets. Its hybrid model—chip manufacturing and patent licensing—creates a highly profitable structure.

Beyond phones, Qualcomm is expanding rapidly in automotive and IoT, generating >$1 billion quarterly from automotive and targeting >20% annual growth.

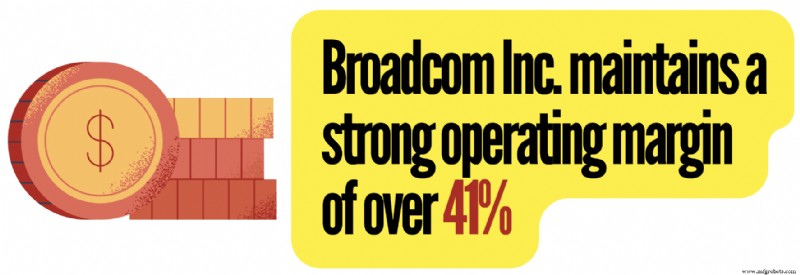

3. Broadcom: Backbone of Global Data Infrastructure

Founded 1961

Core Products: Custom AI accelerators, networking chips

Annual Revenue: $68.2 billion+

Competitive Edge: Custom AI chip leadership

Broadcom excels in networking, custom silicon, and infrastructure software. Its custom AI chips for Google, Meta, and others drive tailored performance at scale.

FY 2025 revenue rose 24% YoY, generating $26.9 billion in free cash flow. 57% of revenue is semiconductor; 43% comes from infrastructure software.

AI revenue hit $20 billion in 2025, growing ~65% YoY. Broadcom projects >$100 billion in AI chip revenue by 2027, deploying 10 GW of custom accelerators across six major customers. [10]

2. Intel: Legacy Chip Giant Reinventing Itself

Founded 1968

Core Products: CPUs, AI accelerators, FPGAs

Annual Revenue: $52.8 billion+

Competitive Edge: Integrated manufacturing

Intel pioneered the first commercial CPU and drove Moore’s Law for decades. It remains the leader in PC and server CPUs, supplying OEMs like Dell, HP, and Lenovo.

Its IDM model—designing and manufacturing its own chips—sets it apart. Recent shifts focus on foundry services (Intel Foundry) and advanced nodes like Intel 18A, while expanding into AI and edge computing.

Key Insight: Annual R&D spend reaches $13.8 billion; capital expenditures exceed $14.6 billion to rebuild manufacturing leadership. [11]

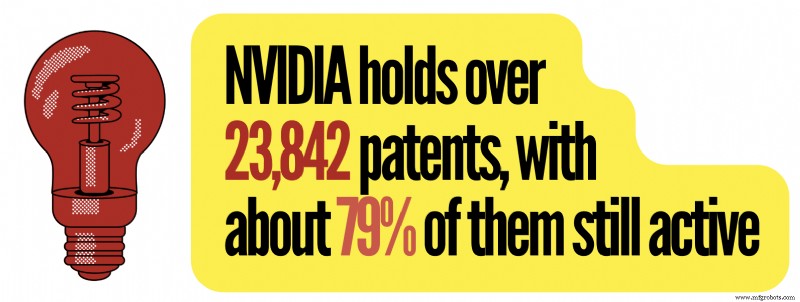

1. NVIDIA: Center of the AI Revolution

Founded 1993

Core Products: GPUs, data‑center systems, AI software platforms

Annual Revenue: $215 billion+

Competitive Edge: CUDA ecosystem

NVIDIA has transformed from a gaming graphics pioneer to the dominant AI computing provider, powering ChatGPT, autonomous vehicles, robotics, and cloud services. It could tap a cumulative AI revenue opportunity of up to $1 trillion.

Its GPUs dominate 75% of the world’s TOP 500 supercomputers, underscoring its leadership in scientific and enterprise computing.

CUDA, a proprietary software stack, creates significant switching costs for developers, cementing NVIDIA’s market dominance.

Key Insight: NVIDIA controls ~92% of the discrete GPU market and ~80% of the AI accelerator market. [13]

Read More

- 14 Leading Japanese Semiconductor Companies

- 16 Top Chinese Semiconductor Companies

- 15 Quantum Processors That Feature a New Computing Paradigm

Sources Cited and Additional References

- What the Chips and Science Act means for AI, Stanford University

- Marvell projects strong fiscal 2028 revenue on AI‑driven data center boom, Reuters

- Analog Devices has the strongest growth outlook among DAO peers, Seeking Alpha

- Fourth quarter and fiscal 2025 financial results, Analog Devices

- Unlocking innovation while tackling availability & obsolescence, Converge

- Applied Materials’ patents and statistics, GreyB

- AI memory is sold out, causing an unprecedented surge in prices, CNBC

- Analog semiconductor market innovations shaping next‑gen technologies, Precedence Research

- AMD valuation premium looks different after the latest earnings beat, Investing.com

- Broadcom Inc. Q4 2025 earnings call highlights, Yahoo Finance

- The latest advancement in Intel Foundry process technology, Intel

- 23 Fastest supercomputers in the world, RankRed

- NVIDIA controls 92% of the GPU market, Carbon Credits

Industrial Technology

- Karkhana.io Solves Manufacturing Challenges for Kitchen Automation Startups

- CNC Machining vs. Die Casting: Selecting the Optimal Process for Your Parts

- Swanton Welding Expands Workforce: Careers in Fabrication & Welding

- Step‑by‑Step Guide: Wiring a 3‑Phase & 1‑Phase 400V/230V Distribution Board (UK & EU)

- Balance Speed and Security: Avoid Compromising Safety for Faster Delivery

- Choosing the Right Social Platform: Facebook, LinkedIn, or Twitter for Industrial Businesses

- Ensuring Trustworthy Supply‑Chain Data: A Proven Strategy

- Choosing a Trusted Medical CNC Machining Manufacturer: A Comprehensive Buyer’s Guide

- AI & IoT Fuel Digital Twins for Smarter Supply Chains

- 5 Essential Advantages of Predictive Maintenance in Manufacturing