Marvell Technology’s 11 Key Competitors: Shaping AI, Cloud, and Semiconductor Markets in 2026

Over the past decade, Marvell Technology has become a pivotal player driving the global AI and data‑center revolution. From its roots in storage and networking chips, the company has evolved into a leading provider of custom AI silicon, high‑speed networking solutions, optical interconnects, and cloud‑infrastructure semiconductors.

The transformation is remarkable. While a few years ago Marvell’s revenue was dominated by storage and networking products, the data‑center segment now accounts for more than 75% of total sales, positioning it as the firm’s primary growth engine. The company projects its custom AI silicon business alone to surpass $10 billion in annual revenue by 2029【1】.

2026 proved to be a breakout year: Marvell’s share price more than tripled, earning a coveted spot in the S&P 500 Index. Yet as the semiconductor ecosystem expands, competition among chipmakers is intensifying.

The table below outlines the 11 most influential competitors, highlighting their core strengths and how they are driving the future of AI, cloud computing, and semiconductor technology.

Did you know? Marvell estimates that its addressable market in data‑center infrastructure will more than triple by 2028【2】.

11. Credo Technology

Founded: 2008

Core Products: Ethernet DSPs, PCIe connectivity solutions

Annual Revenue: $1.34 billion+

Competitive Edge: Advanced SerDes, DSPs, and Active Electrical Cables (AECs)

Credo has rapidly become a high‑growth semiconductor company, fueled by the AI infrastructure boom. Its focus on efficient data movement between AI accelerators, networking gear, and storage systems addresses a critical bottleneck as bandwidth demands rise from 400 G to 800 G and 1.6 T networking.

Credo’s AECs deliver a lower‑cost, energy‑efficient alternative to optical interconnects, gaining traction with hyperscalers building AI data centers【3】. In FY 2026, the company reported a 126% year‑over‑year revenue increase.

10. Astera Labs

Founded: 2017

Core Products: Scorpio Fabric Switches, Aries PCIe Retimers

Annual Revenue: $1 billion+

Competitive Edge: AI connectivity infrastructure (PCIe, CXL)

While NVIDIA and AMD dominate AI compute, Astera Labs specializes in the connectivity layer that scales those systems. Its semiconductor solutions reduce bottlenecks between processors, accelerators, memory, and storage, boosting performance, efficiency, and scalability.

Astera’s focus on PCIe and Compute Express Link (CXL) positions it at the forefront of next‑generation AI systems, where shared memory and resource utilization are critical. Marvell also invests heavily in advanced connectivity technologies, creating direct competition.

The company is expanding its Scorpio Fabric Switch portfolio to support ever‑larger AI clusters, improving bandwidth and scalability across rack‑scale deployments.

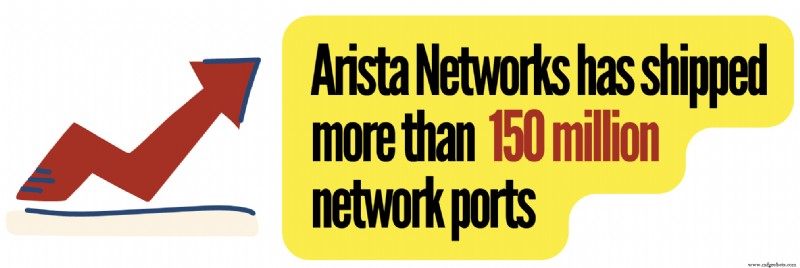

9. Arista Networks

Founded: 2004

Core Products: AI Ethernet Fabrics

Annual Revenue: $9.71 billion+

Competitive Edge: Extensible Operating System (EOS)

Arista was built for cloud computing from the outset. Its EOS delivers a software‑centric architecture that enhances reliability, automation, and scalability【4】, winning traction with hyperscalers such as Microsoft and Meta.

Arista’s high‑speed Ethernet platforms serve as a preferred alternative to proprietary networking solutions, enabling cloud providers to scale AI infrastructure more efficiently.

Unlike Marvell, which supplies merchant silicon and networking components, Arista offers end‑to‑end networking systems and software platforms, but both target AI networking budgets and data‑center connectivity.

Financially, Arista is one of the most profitable networking vendors, with gross margins above 60% and operating margins near 46%—levels rarely seen in the industry.

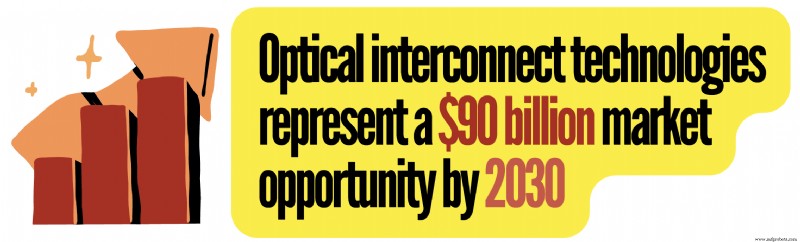

8. Lumentum Holdings

Founded: 2015

Core Products: Optical Engines, Data‑Center Optics

Annual Revenue: $2.48 billion+

Competitive Edge: Advanced laser technology expertise

Lumentum competes with Marvell in optical networking infrastructure, supplying lasers, optical engines, transceivers, and coherent communication technologies that link GPUs, CPUs, storage, and networking gear in modern AI data centers.

In 2022, Lumentum acquired NeoPhotonics, expanding its high‑speed optical capabilities and enhancing its position with hyperscale customers developing AI networks.

Today, Lumentum’s coherent optical technologies directly compete with portions of Marvell’s optical networking portfolio, especially in high‑speed interconnect deployments.

It is actively developing 800 G, 1.6 T, and future optical networking architectures, ensuring relevance as data‑center bandwidth requirements grow【5】.

7. Alchip Technologies

Founded: 2003

Core Products: AI accelerators, Data‑Center ASICs

Annual Revenue: $990 million+

Competitive Edge: Pure‑play ASIC focus, 2.5D/3DIC chiplet packaging

Alchip has benefited from the AI boom, as hyperscalers increasingly design custom AI hardware rather than relying solely on merchant processors. Unlike mainstream chipmakers, Alchip’s core service is helping clients design, fabricate, and ship fully custom chips.

Its close partnership with TSMC allows rapid migration to advanced nodes, including 3 nm and beyond. While Alchip’s revenue is smaller than Marvell’s, its specialization in custom ASIC design makes it a direct competitor in that niche.

6. Coherent Corp

Founded: 1971

Core Products: Coherent Optical Engines, Data‑Center Optics

Annual Revenue: $6.60 billion+

Competitive Edge: Leadership in photonics, vertical integration

Coherent specializes in photonics, lasers, optical communications, and advanced materials, enabling massive data transmission across modern networks. With AI demanding unprecedented bandwidth, Coherent has become a key supplier to hyperscale data centers, reporting $6.6 billion in FY 2026 revenue—a 18% year‑over‑year growth【6】.

Unlike Marvell, Coherent does not compete heavily in custom AI ASICs or merchant Ethernet switching silicon, focusing instead on optical infrastructure. Its vertical integration—from laser manufacturing to complete modules—provides quality control, reduces supply‑chain risk, and accelerates product development.

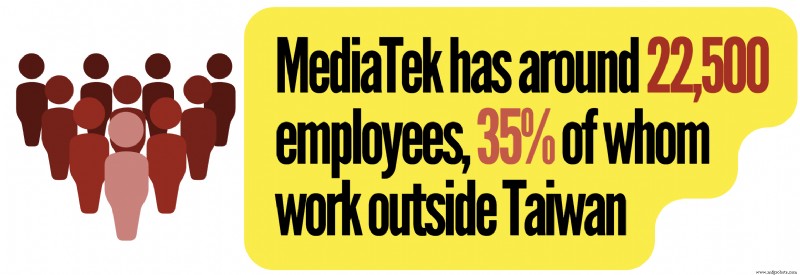

5. MediaTek

Founded: 1997

Core Products: AI accelerator and data‑center ASICs

Annual Revenue: $19.23 billion+

Competitive Edge: Massive smartphone scale, close ties with TSMC

MediaTek has become a significant competitor to Marvell, especially in custom AI ASICs. It has aggressively expanded into hyperscaler‑designed AI chips, a market Marvell considers a key growth opportunity. MediaTek estimates the AI ASIC market could reach $80 billion by 2027, targeting a 10‑15% share.

MediaTek also invests in high‑speed SerDes, advanced packaging, and chiplet architectures—addressing the same AI infrastructure bottlenecks as Marvell. The company is developing next‑generation 224 G SerDes technology, a critical component for efficient data movement in AI systems.

4. Qualcomm

Founded: 1985

Core Products: Custom AI Silicon, Server CPUs

Annual Revenue: $44.49 billion+

Competitive Edge: Wireless technology leadership, vast patent portfolio

Qualcomm has diversified into automotive, AI, industrial IoT, PCs, and data‑center infrastructure, making AI a top priority. Its Snapdragon X Elite platform launched a new generation of AI PCs, while its on‑device AI engines run large language models without relying solely on cloud infrastructure.

In 2025, Qualcomm acquired Alphawave Semi for $2.4 billion, bringing high‑speed connectivity, SerDes, chiplet interconnects, and networking IP—areas where Marvell has traditionally excelled.

Qualcomm’s patent portfolio—over 334,800 patents and applications—generates more than $5.6 billion in licensing revenue, providing a stable high‑margin income stream.

3. Cisco Systems

Founded: 1984

Core Products: Silicon One Networking Platforms

Annual Revenue: $60.75 billion+

Competitive Edge: Deep relationships with enterprise IT departments

Cisco benefits from the broader AI ecosystem: every AI data center requires networking, security, optics, routing, and data‑management infrastructure. Cisco’s Silicon One chips, Nexus switches, optical networking, and security platforms give it a strong presence across AI infrastructure.

While Marvell supplies Ethernet switch silicon and networking chips, Cisco builds complete networking systems, increasingly powered by its own Silicon One architecture. Both companies compete for spending on high‑speed networking and data movement.

Optical networking is a major battleground. Cisco’s acquisition of Acacia Communications yielded over $1 billion in orders in a single FY 2026 quarter and is projected to grow by more than 200% year‑over‑year【7】.

2. AMD

Founded: 1969

Core Products: Instinct AI accelerators, EPYC server platform

Annual Revenue: $37.45 billion

Competitive Edge: Xilinx acquisition, adaptive computing

AMD’s data‑center business has been a major success story. Its EPYC processors steadily gained share from Intel in enterprise servers and hyperscale cloud deployments, with data‑center revenue exceeding $19 billion in FY 2026—the largest segment for AMD.

While Marvell focuses on custom AI silicon and networking solutions, AMD supplies AI accelerators, server CPUs, and data‑center platforms. Both target the same hyperscaler AI spending budgets, though their product lines differ.

AMD’s acquisition of Xilinx made it a leader in FPGAs, strengthening its industrial market position. The subsequent acquisition of Pensando added DPUs and cloud networking technologies, expanding AMD’s role in modern data centers.

From a market‑cap perspective, AMD grew from under $2 billion in 2015 to over $800 billion in 2026—a remarkable comeback story【8】.

1. Broadcom

Founded: 1961 (as HP Associate division)

Rival Products: Custom AI ASICs, Ethernet Switch chips

Annual Revenue: $75.47 billion+

Competitive Edge: Scale and financial strength

Broadcom’s unique strength lies in dominating unseen markets. While NVIDIA garners attention for GPUs, Broadcom supplies the networking and connectivity backbone that enables AI clusters to scale. It is Marvell’s most direct competitor, engaging in head‑to‑head battles in custom AI silicon—one of the fastest‑growing semiconductor segments.

In networking, Broadcom’s Tomahawk and Jericho product families directly challenge Marvell’s Teralynx switching platforms. Networking accounted for nearly 40% of Broadcom’s AI semiconductor revenue in FY 2026, underscoring the market’s strategic importance.

Broadcom’s key advantage is its sheer size. With annual revenue exceeding $75 billion versus Marvell’s $8.1 billion, it can invest roughly $12 billion annually in R&D and maintain deep relationships with major cloud providers. The company also aims to exceed $100 billion in annual AI chip revenue by FY 2027【9】【10】.

Read More

- 16 Leading Chinese Semiconductor Companies

- 14 Nvidia Competitors and Alternatives

Sources Cited and Additional References

- Marvell sees custom chip revenue topping $10 billion by 2029, Reuters

- Marvell data center revenues surge, but the rest fall, MarketBeat

- Can Credo Technology maintain revenue growth amid the AI boom? Yahoo Finance

- EOS is the modern cloud network operating system, Arista

- Lumentum gains from traction in transceivers, Yahoo Finance

- Coherent’s revenue throughout the years, Macrotrends

- Earnings transcript of Cisco, The Motley Fool

- Lisa Su saved AMD. Now she wants Nvidia’s AI crown, Forbes

- Broadcom’s R&D expenses throughout the years, Macrotrends

- Broadcom shares slide despite jump in revenue on AI chip demand, WSJ

Industrial Technology

- Understanding Series and Parallel Circuits: How They Work and Why They Matter

- 50 Proven Facilities Management Tips & Best Practices

- 50 Essential Inventory Control Resources: Master Inventory Management with Top Articles, Tutorials & Videos

- Brazing Explained: Join Metal Parts Safely and Effectively

- High‑Performance Variable Voltage & Current Power Supply – Stable Output for Lab and Industrial Use

- U.S. Navy Turns 248: From Philadelphia Foundations to Global Maritime Power

- DIACs Explained: Design, Functionality, and Key Applications

- Mastering Flex‑Rigid PCB Assembly: Simplify Processes & Enhance Reliability

- Choosing the Right Dust Collector Fire Suppression System: 3 Proven Types

- Why Tungsten Lamps Still Power Automotive Turn Signals