STMicroelectronics: Powering Tesla’s EVs and Apple’s 5G Sensors

In many sectors, a few key customers can drive a company's growth. For STMicroelectronics, success in automotive and consumer electronics hinges on Tesla and Apple.

Yole Développement’s imaging, compound semiconductor and power electronics teams provide a snapshot of ST’s penetration and achievements in these two arenas, focusing on its power devices and image sensors.

Automotive & e‑Mobility

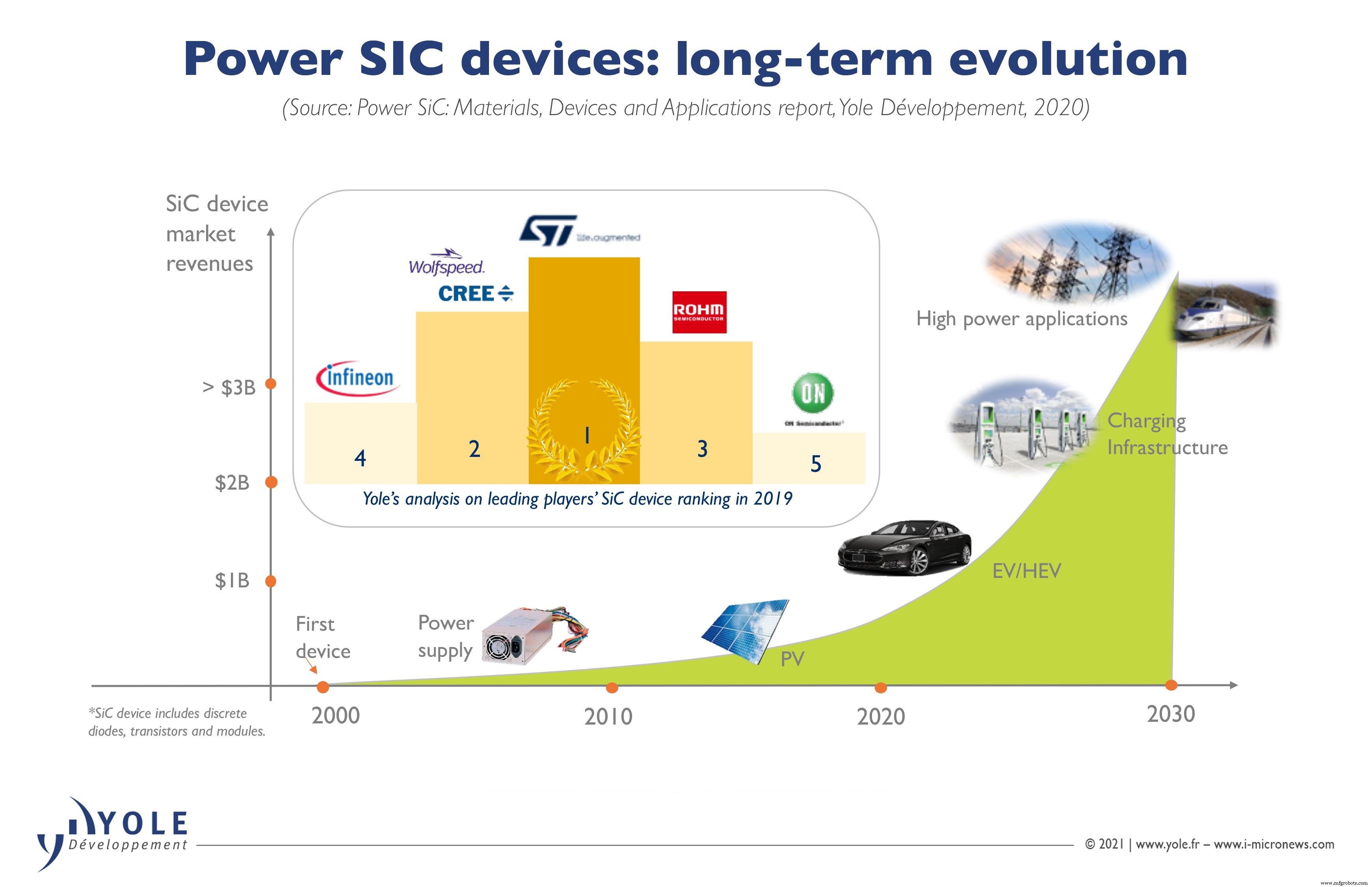

For STMicroelectronics and Tesla, silicon carbide (SiC) has always been the cornerstone. In 2018, Tesla became the first premium automaker to integrate a full SiC power module into the traction motor of its Model 3. A teardown from System Plus Consulting revealed that the small, high‑power‑density inverter module was built around STMicroelectronics’ SiC MOSFETs – cementing a partnership that would shape both companies’ futures in EV power electronics.

Since that breakthrough, the SiC market for automotive applications has expanded rapidly. Tesla’s adoption signaled to other OEMs that SiC could meet the reliability demands of safety‑critical traction inverters, prompting global manufacturers to accelerate SiC development for e‑mobility.

ST manufactures modules for key vehicle blocks, including traction inverters, onboard chargers and DC‑to‑DC converters. Proving traction inverter technology with Tesla remains pivotal, as this segment delivers the highest revenues and growth potential. In contrast, onboard chargers are limited to plug‑in hybrids and battery electric vehicles, while DC‑to‑DC converters involve lower‑power conversion.

Thanks largely to Tesla, ST now enjoys a strong foothold in the burgeoning e‑mobility market and stands as the leader in SiC power devices. Partnerships such as the Renault‑Nissan‑Mitsubishi Alliance for onboard chargers and a recent deal with Chinese BYD have further boosted Q4 performance. Yole’s analysis confirms ST as Tesla’s top SiC supplier.

SiC wafer supply constraints have posed challenges for many players, including Cree, Rohm, Infineon, ON Semiconductor, Mitsubishi Electric and STMicroelectronics. To address shortages, ST expanded capacity and secured long‑term agreements. In December 2019, it acquired Swedish wafer manufacturer Norstel, enabling the company to supply more than 40 % of its internal production by 2024 and to invest in 8‑inch wafer R&D, positioning it for the industry’s shift to larger substrates.

Apple Drives 5G Mobile & Consumer Tech

While the automotive strategy delivers solid returns, ST’s financials are also buoyed by Apple. Though a relatively small player in CMOS image sensors (CIS), ST captured 6 % of the $19.3 billion CIS market in 2019 – enough to rank fourth behind Sony, Samsung and OmniVision. ST’s expertise in 3‑D imaging and sensing underpins Apple’s 5G ambitions.

In 2017, ST supplied near‑infrared (NIR) sensors for the iPhone X’s true‑depth camera and a time‑of‑flight (ToF) proximity detector with flood illuminator. Today, the company supplies ToF detectors and NIR CMOS sensors to the iPhone 12 series, contributing to Q3 2020 sales. Production bottlenecks shifted Apple’s manufacturing to Q4, further lifting ST revenue.

ST’s multi‑zone ToF detectors also appear in Samsung’s Galaxy S21, diversifying its consumer revenue. Unlike U.S. competitors, ST has largely avoided Huawei trade‑ban impacts, even securing a license to build devices for the Chinese giant – a potential source of future production.

Capacity remains a risk. Sony’s direct ToF sensor has recently been integrated into Apple’s iPad Pro and the latest iPhone 12, and more Sony devices are expected. While ST continues to secure foundry space for many systems, Yole notes that the company has yet to adopt a similar strategy for CIS products, potentially limiting future growth.

Despite these uncertainties, ST’s Q4 2020 results were robust. Whether it can secure additional Tesla and Apple deals remains to be seen, but its revenue dynamics are clearly intertwined with these industry leaders for the foreseeable future.

This article is based on analysis originally published by Yole Développement.

Pierre Cambou MSc, MBA, is a principal analyst in the photonics and sensing division at Yole Développement (Yole). He is dedicated to imaging related activities by providing market & technology analyses along with strategy consulting services to semiconductor companies. At Yole, Pierre is responsible for the CIS Quarterly Market Monitor, and has authored more than 15 Yole Market & Technology reports. Pierre has an Engineering degree from Université de Technologie de Compiègne (France) and a Master of Science from Virginia Tech (VA, USA). Pierre also graduated with an MBA from Grenoble Ecole de Management (France).

Ezgi Dogmus, PhD. is team lead analyst in compound semiconductor & emerging substrates activity within the power & wireless division at Yole. She manages the expansion of the technical expertise and the market know-how of the company. In addition, Ezgi actively assists and supports the development of dedicated market & technology reports, as well as custom consulting projects. After graduating from University of Augsburg (Germany) and Grenoble Institute of Technology (France), Ezgi received her PhD. in Microelectronics at IEMN (France).

Milan Rosina, PhD, is principal analyst, power electronics and batteries, at Yole, within the power & wireless division. He is engaged in the development of the market, technology and strategic analyses dedicated to innovative materials, devices and systems. His main areas of interest are EV/HEV, renewable energy, power electronic packaging and batteries. He received his PhD degree from Grenoble Institute of Technology (Grenoble INP) in France.

Ana Villamor, PhD serves as a technology & market analyst, power electronics & compound semiconductors within the power & wireless division at Yole. She is involved in many custom studies and reports focused on emerging power electronics technologies at Yole, including device technology and reliability analysis (MOSFET, IGBT, HEMT, etc). She holds an Electronics Engineering degree completed by a Master and PhD. in micro and nano electronics from Universitat Autonoma de Barcelona (SP).

Related Contents:

- Electrification, EVs and battery management: an interview with NXP

- Safely controlling an EV traction inverter

- Fourth‑generation global shutter explained, and why embedded image sensors need better performance metrics

- New ams image sensors for high throughput industrial vision

- Embedded sensors are key to smart mobility growth

For more Embedded, subscribe to Embedded’s weekly email newsletter.

Embedded

- Integrating Qt with DDS: Building Scalable IoT Applications

- OPC UA & DDS Forge Unified Partnership with IIC and Industrie 4.0

- Molybdenum Mining & Processing: From Ore to Metal – A Technical Overview

- Stainless Steel Explained: Composition, Production, and Global Impact

- Apple AirTags in the IoT Landscape: What Businesses Need to Know

- Microsoft Ignite 2023: IoT, Robotics, and the Future of Industry 4.0

- Exploring 6G: The Future of Ultra-Fast Connectivity

- Copper Brazing Explained: Techniques & Tips for Strong, Reliable Connections

- How IoT & Industrial Automation are Powering Manufacturing Innovation

- Master Copper Brazing: A Complete Guide to Joining Tubes & Fittings