Automotive Semiconductor Shortage: How Industry Pressures Are Shaping the Supply Chain

Michael Knight, president of TSG, explains the multi‑year, multi‑factor origins of the automotive semiconductor crunch.

In 2020, the global economy began to recover from the COVID‑19 shock. Electronics manufacturers, having learned to adapt, positioned themselves for a post‑pandemic surge. By early 2021, headlines focused on semiconductor shortages and their ripple effect across consumer electronics and the automotive sector. While the car market had been under‑produced pre‑pandemic, vehicle sales steadied and then climbed, forcing manufacturers to back‑order parts—including the growing share of electronic components.

Figure 1. Rising vehicle sales increase dealer inventory pressure and demand on automotive suppliers.

Lead times for semiconductors have dominated the conversation, yet other electronic parts such as high‑capacitance ceramic capacitors, power inductors, and high‑temperature connectors are also in short supply. A single missing component can halt an entire production line, so even a nominal chip surplus would not resolve the bottleneck.

Drivers of Component Demand

The electronic content of new vehicles is expanding rapidly—especially for hybrids and fully electric models. Production of EVs is projected to double to over 12 million units per year in the next few years, driving a 30‑50% increase in electronics per vehicle. Figure 2 illustrates the projected growth of EVs and the resulting spike in component demand.

Figure 2. Forecasted exponential growth in electric vehicles heightens the need for electronic components.

Many automotive parts are custom‑designed and cannot be scaled up overnight. Expanding production capacity often takes quarters to years, especially for semiconductors that rely on older fabrication nodes. Chipmakers prioritize newer, higher‑margin technologies, leaving older processes under‑utilized.

Broader Electronics Demand

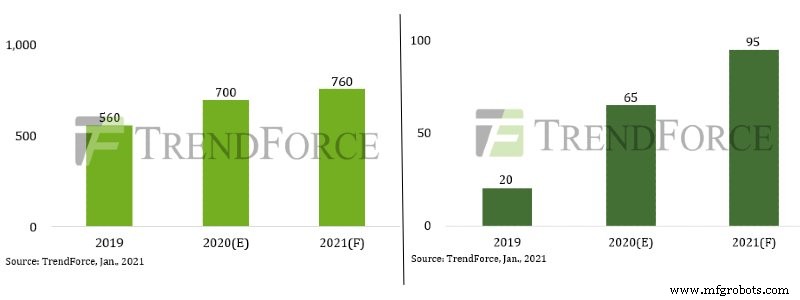

The surge in component consumption is not limited to transportation. Consumer electronics, telecommunications, and computing are all driving increased demand. For instance, 5G smartphones now use roughly 50% more ceramic capacitors than their 4G predecessors, and notebook production rose 22% last year as remote work surged.

Figure 3. Growth of TDDI IC shipments for smartphones and tablets from 2019 to 2021. Units in millions. Image courtesy of TrendForce.

Manufacturers that serve the automotive market also supply these other sectors. When demand across all verticals peaks, they must prioritize customers, often favoring higher‑margin or larger‑volume buyers. Automakers, with their long product life cycles and aggressive procurement terms—such as just‑in‑time inventory, low liability, and financial penalties for delays—exert significant pressure on suppliers.

Shifting Supplier Capacity

During the pre‑pandemic slowdown, component producers reallocated capacity to higher‑margin consumer electronics. When automakers surged back, the anticipated supply was already absorbed by other sectors, leaving no buffer for the automotive industry’s just‑in‑time model.

Additional complications arise from U.S.–China trade tensions, making price‑sensitive U.S. automakers increasingly reliant on Chinese suppliers. Coupled with more frequent severe weather events that disrupt global supply chains, the sector faces a “perfect storm” that has already cost the industry billions in lost sales and profits.

Global Supply Chain Fragility

Automotive supply chains are notoriously complex. A survey by Jabil Electronics found that an average automaker relies on 250 tier‑one suppliers and up to 18,000 suppliers across its extended network. Each link can be affected by fire, flood, earthquake, political unrest, tariffs, or disease, underscoring the fragility of the current system.

Short‑term fixes are unlikely. The industry must brace for significant revenue losses—estimated at $61 billion in lost sales—while restructuring its supply chain to withstand future shocks.

Industry Articles are a form of content that allows industry partners to share useful news, messages, and technology with All About Circuits readers in a way editorial content is not well suited to. All Industry Articles are subject to strict editorial guidelines with the intention of offering readers useful news, technical expertise, or stories. The viewpoints and opinions expressed in Industry Articles are those of the partner and not necessarily those of All About Circuits or its writers.

Embedded

- Navigating the Automotive Technician Shortage: A New Career Path

- Plastics: Driving the Future of Automotive Hardware Innovation

- Semitron® MPR1000: The Next‑Generation Material for Semiconductor Plasma Processing

- Revolutionizing Supply Chains to End the Global Semiconductor Shortage

- NX Series: Modular Machining Centers for Automotive Production Lines

- Revolutionizing Mass Production: The Key Advantages of 3D Printing

- Cutting Automotive Production Costs: Proven Strategies for OEMs & Tier Suppliers

- Top Innovations Transforming Industrial Maintenance

- Precision CNC Milling: Crafting High-Quality Automotive Components

- Why Collaborative Robots Are Essential for Modern Metal Stamping & Punching