Additive Manufacturing Worldwide: Current 3D Printing Adoption in North America & Europe

Check out Part 2 of the AM Around the World series, which explores the adoption of 3D printing in the APAC region.

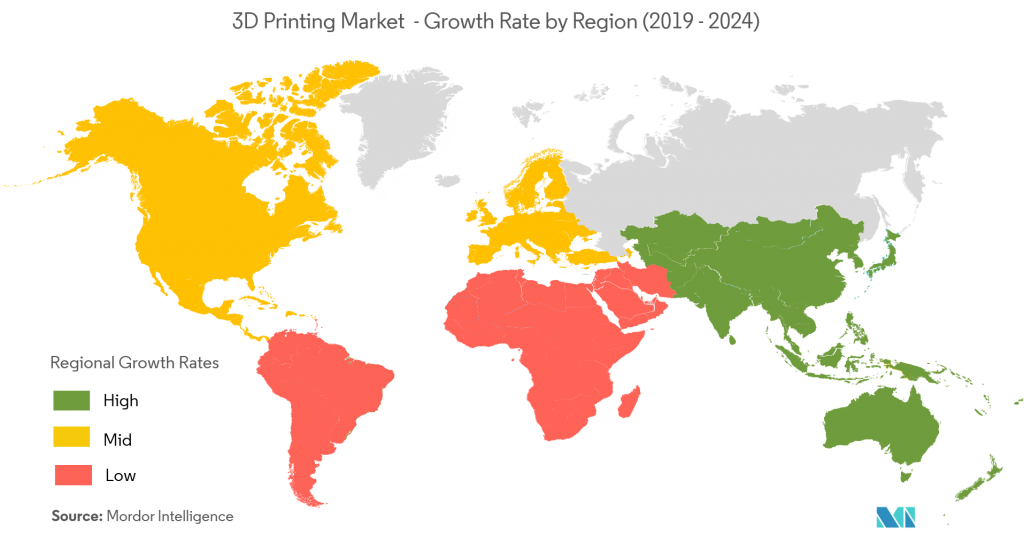

North America and Europe still dominate the additive manufacturing (AM) market, hosting the largest share of industrial 3D‑printing firms and the most patents. However, the region’s lead is under threat from Asia’s rapid growth.

How is the 3D‑printing industry evolving in these regions, and what strategies can secure their competitiveness?

3D‑Printing Adoption in North America

North America leads the AM market, holding 35 % of installed industrial systems, according to the 2019 Wohlers Report.

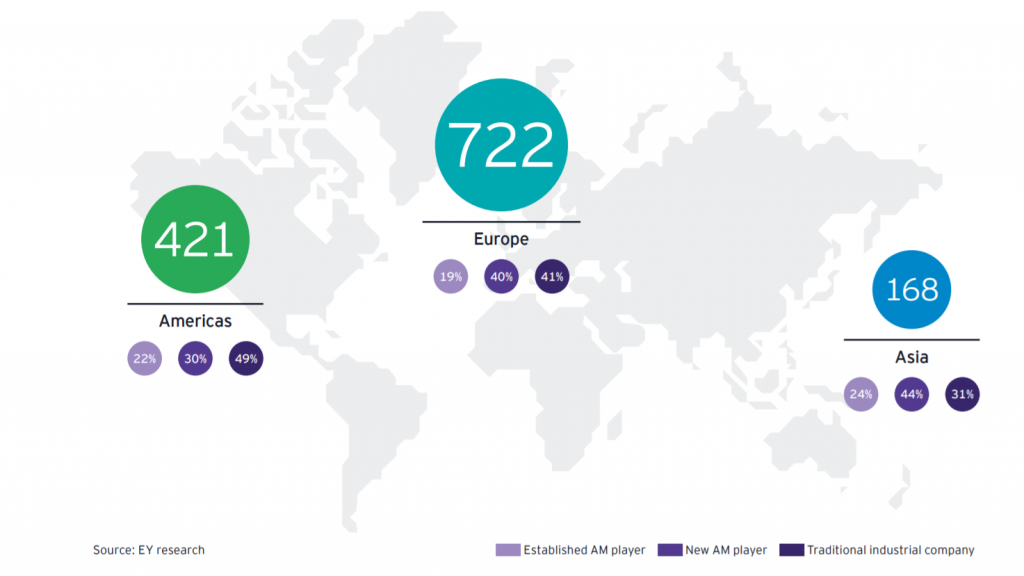

The United States is the primary driver, supported by a robust ecosystem of industry leaders, startups, and a high volume of patents. EY reports that 29 % of all global AM companies are headquartered in the U.S., including established names like 3D Systems and Stratasys, unicorns such as Carbon, Desktop Metal, and Formlabs, and traditional manufacturers like GE and HP that have embraced AM.

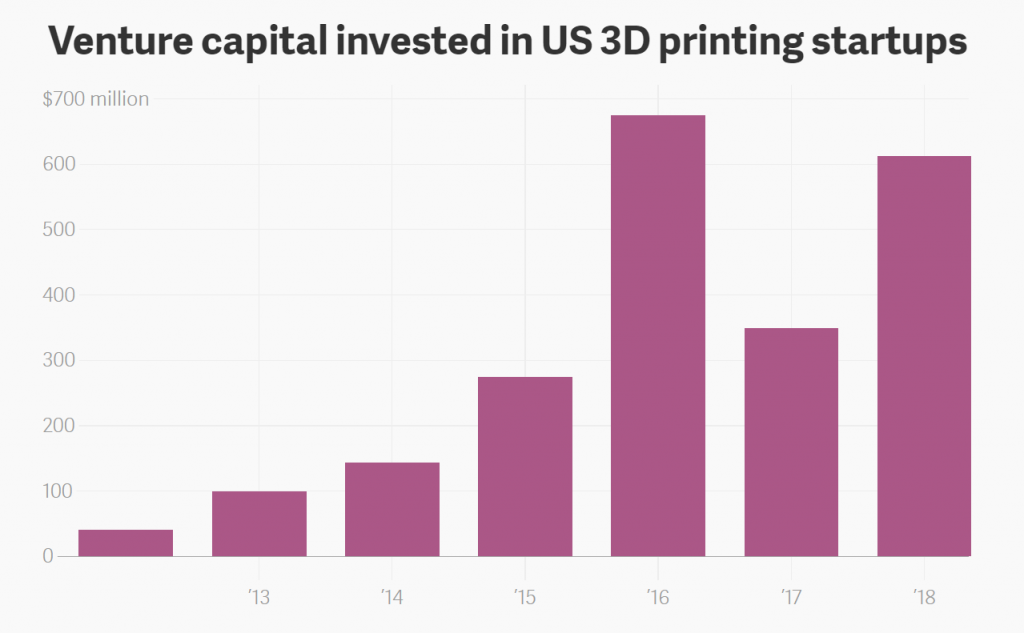

U.S. start‑ups secured over $600 million in venture capital in the first half of 2018—more than the total raised from 2012‑2015 combined—highlighting the region’s entrepreneurial momentum.

The U.S. Government’s Role in AM Industrialisation

While private investment fuels most innovation, the federal government has launched key initiatives such as the National Additive Manufacturing Innovation Institute (NAMII) in 2012, later rebranded as America Makes. Today, America Makes coordinates 88 R&D projects and serves as a hub for advanced manufacturing innovation.

In partnership with ANSI, America Makes produced the first AM Standardisation Roadmap, a framework that identifies existing standards, gaps, and priority areas for new development. The roadmap helps harmonise standards, reduce barriers, and accelerate adoption across industries.

Is the U.S. Losing Its Edge?

Despite its leadership, the U.S. faces competition from South Korea, the UK, and Germany. A.T. Kearney notes that the U.S. lacks a cohesive national AM strategy, with lower government support in 2017 compared to the global average. While the 2018 White House strategy on advanced manufacturing does not specifically address AM, recent defense‑related funding—$6 million from the Air Force for 3D‑printed rocket engines and $13.2 billion in 2018 for technology innovation—demonstrates targeted support.

Private Companies Drive AM Growth

By 2019, more than half of U.S. companies had adopted 3D printing, and 22 % were planning future adoption. Aerospace, industrial goods, medical, and automotive sectors—led by firms such as Ford ($45 million investment in its Advanced Manufacturing Center) and GM—are key adopters. A 2019 Sculpteo survey found that North American firms plan to boost AM investment by at least 50 %.

To sustain leadership, U.S. policymakers must expand workforce development, education, and incentive programs that encourage broader commercial adoption.

3D‑Printing Adoption in Europe

Europe holds the second‑largest AM market share, with 55 % of global AM firms headquartered in the region, per EY. The continent is home to leading manufacturers such as EOS, Renishaw, SLM Solutions, Ultimaker, and Photocentric.

Western European countries—Germany, the UK, Italy, and France—drive AM development. IDC surveys confirm these nations lead in adopting AM for end parts, especially in aerospace and healthcare. Several have national AM strategies integrated into their Industry 4.0 plans.

Eastern Europe, notably Russia, possesses significant potential but lags in R&D and industrial deployment. Russian initiatives aim to develop AM technologies, yet practical manufacturing adoption remains limited.

According to CECIMO’s 2018 report, skill shortages are the primary barrier, with 52 % of respondents citing difficulty hiring competent AM staff. Key expertise gaps include quality assurance, testing, and regulatory compliance—critical for series production.

Country Spotlight: Germany

Germany, the EU’s manufacturing hub, launched its ‘Industrie 4.0’ initiative in 2011, incorporating AM as a core technology. With 148 research institutions—led by the Fraunhofer Institute—Germany drives innovation. Fraunhofer’s FutureAM project (2017) aims to scale metal AM through advanced technologies; recent results include a new optical system for L‑PBF that can produce large metal components up to ten times faster than conventional systems.

The Additive Manufacturing Association within VDMA supports industrialisation, with 150 members spanning suppliers, software, materials, and end‑users. Their roadmap targets materials logistics, environmental and safety standards, data processing, and process standardisation.

Siemens’ 3‑year IDEA project, funded by the German Ministry of Education and Research, focuses on integrating digital twins with AM to enhance industrial deployment.

Current adoption shows that only 13 % of 560 German companies surveyed by VDI use AM for complete end‑use products, though a third incorporate AM components into their production—an encouraging trend. The automotive sector is a key growth driver, with BMW’s IDAM project aiming to mass‑produce 50 000 components annually via AM.

Country Spotlight: United Kingdom

The UK is a global leader in AM research and application, ranking second in Europe after Germany. The 2017 Industrial Strategy outlines a clear path to elevate the UK as a top AM player.

UK universities—Nottingham, Sheffield, and Cambridge—are research powerhouses. The Manufacturing Technology Centre, opened in 2015, houses a national AM facility.

Commercial adoption, however, remains uneven. While firms such as Bowman International and Renishaw employ AM for specific parts, most UK manufacturers have yet to fully embrace the technology. Barriers include skill shortages, limited government understanding, cautious investment attitudes, and fragmented support structures.

With a strong knowledge base and advanced manufacturing capacity, the UK can expand its AM supply chain, provided there is coordinated government action to translate research into commercial deployment.

Maintaining a Competitive Edge: North America & Europe

In 2019, North America and Western Europe remained leaders, with Germany and the U.S. driving most AM advances. Yet global uncertainties—Brexit, U.S.‑China trade tensions—threaten momentum.

The EU’s recent commitment to prioritise AM in U.S. trade talks seeks to eliminate non‑tariff barriers and create unified certification standards, easing market entry for AM solutions across both regions.

To preserve their leadership, policymakers and industry must intensify AM education, incentivise adoption, and foster a robust ecosystem that can compete with Asia’s rapidly expanding market.

3D printing

- 3D Printing vs Additive Manufacturing: Understanding the Key Differences

- The Internet of Things in Additive Manufacturing: What It Means for Customers, Data, and Operations

- Generative Design & 3D Printing: Building Tomorrow’s Manufacturing

- AM Around the World: Asia‑Pacific 3D Printing Maturity and Rapid Growth

- Top Metal 3D Printing Materials: Unlocking Additive Manufacturing’s Potential

- Understanding Urethane: Global Uses and Key Advantages

- Additive Manufacturing 101: A Beginner’s Guide to 3D Printing

- Revolutionizing Medicine & Dentistry: The Power of Additive Manufacturing

- How Selective Laser Sintering (SLS) Converts 3D CAD Designs into Solid Parts

- Mastering 3D Printer Flow: Definition, Significance, and Calibration Tips