AI Chip Startups Plateau as Industry Focus Shifts to In-House Solutions

While the tech industry celebrates an AI renaissance, the influx of AI chip startups has plateaued. Established hyperscalers such as Google, Amazon, and Meta are now building proprietary processors that meet their specific workloads, raising the barrier to entry for new players in the datacenter market.

Machine‑learning (ML) technologies continue to evolve rapidly, with new neural‑network architectures emerging across every electronic system.

Laurent Moll, Chief Operating Officer at Arteris, predicts that “everyone will have some form of AI integrated into their SoCs.” This trend benefits Arteris, whose core business is providing Network‑on‑Chip (NoC) IP and development tools that enable companies of all sizes to embed AI seamlessly.

For AI chip startups, however, competition is tightening, making it harder to carve out niche market segments.

EE Times will release next month its “Silicon 100” (2021 edition), an annual list of emerging electronics and semiconductor startups. Author Peter Clarke, who has tracked the industry for two decades, reports that the number of specialized AI‑focused chip startups has flattened compared with the previous year. He warns that the industry may have reached a “peak AI” phase.

In short, the golden era of AI chip startups may be ending.

Kevin Krewell, Principal Analyst at Tirias Research, foresees continued acquisition activity. “The surge in startup funding followed Intel’s purchase of Nervana, signaling to investors a clear exit path,” he notes. “The market currently hosts more AI firms than it can sustainably support. We anticipate that only the most innovative—particularly those exploring analog or optical solutions—will survive. Ultimately, AI/ML workloads will be integrated into larger SoCs or chiplet architectures.”

Laurent Moll

Arteris recently interviewed its newly appointed COO, former Qualcomm VP of Engineering and long‑time Arteris CTO. We asked him to explain the current AI‑chip landscape and the future direction of startups.

Gold rushMoll likened the AI boom to “one of the biggest gold rushes” he has witnessed. The prospectors now include both seasoned silicon developers and newcomers without prior fabrication experience, all vying for a slice of the same pie.

While the expanding developer base and diverse applications benefit Arteris, it creates a different reality for AI chip startups. They now compete not only against peers but also against hyperscalers and automotive OEMs, who are developing custom silicon to support their proprietary systems.

Still in expansion phaseThe AI‑chip market remains in an expansion phase, with continued exploration across the board. However, a “little order” is emerging in the datacenter segment, as hyperscalers take control by designing in‑house accelerators tailored to their own data sets.

Moll explains that hyperscalers possess exclusive data sets and proprietary software stacks, allowing them to optimize silicon for specific workloads. In contrast, smaller startups are pioneering novel SoC architectures, SRAM/DRAM usage, stacking, and optical interconnects to deliver superior AI performance relative to off‑the‑shelf solutions.

Hyperscalers, however, often opt for proven architectures. Google’s TPU exemplifies a design that, while not revolutionary, delivers outstanding performance for its targeted workloads.

When asked whether emerging startups could break into hyperscaler datacenters, Moll was skeptical. “It’s unlikely that small firms will gain a foothold in those environments—or that hyperscalers will acquire them—unless their technology proves indispensable.”

He summarized the hyperscaler mindset: “They know their data sets and desired architecture. When a startup offers a compelling, high‑performance solution, they’ll acquire the IP and the team to enhance their own products.”

Krewell concurs, noting that only startups with “spectacular” achievements, such as Cerebras’ wafer‑sized chip, capture hyperscaler interest. NVIDIA remains the default AI platform due to its ubiquitous software ecosystem and scalability.

What about the edge?Edge AI presents a distinct set of opportunities. The market remains broad, with many players still determining how to apply AI and implement it efficiently.

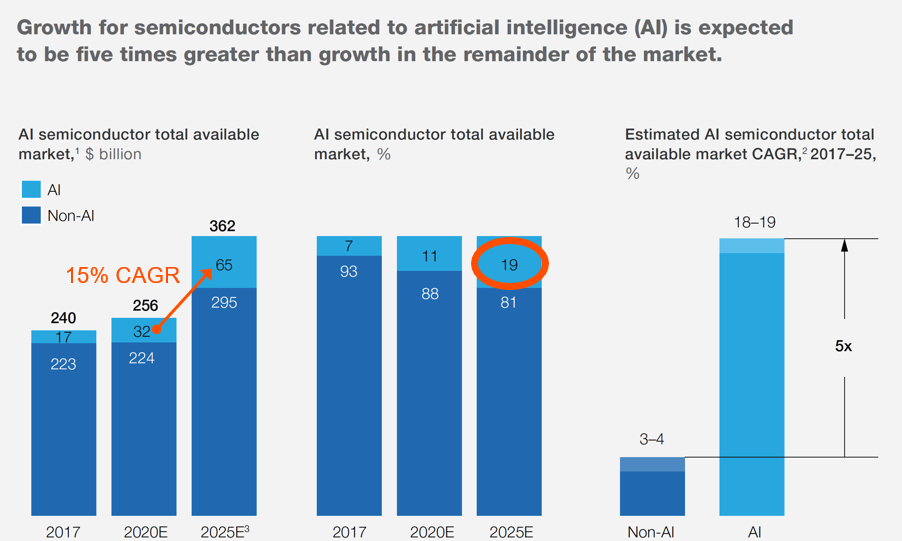

click for full size image

19 percent of the semiconductor TAM will be related to AI/ML in 2025. (Source: Bernstein; Cisco; Gartner; IC Insights; IHS Markit; Machina Research; McKinsey Analysis — Compiled by Arteris)

Krewell highlights that the edge is still largely untapped. Adding ML to sensors and edge devices, especially low‑power analog and in‑memory solutions, shows promise. He foresees significant potential for INT4 and INT2 inference in edge processors, balancing accuracy with minimal power and memory footprints.

Yet the diversity of applications can risk an “Edge AI” hype cycle, as the term lacks a precise definition and is often used generically by startups.

From Moll’s perspective, two edge trends emerge: (1) AI embedded within multifunctional chips—driving the most rapid growth, particularly in smartphones where AI accelerators power voice and vision features; and (2) large dedicated AI chips, which remain an evolving niche.

AI in automotiveIn vehicles, AI adoption spans from advanced driver‑assist systems (ADAS) to full autonomy. Moll envisions a spectrum of solutions—from lightweight computer‑vision chips to large AI processors handling high‑volume inference.

While incumbents with proprietary chips dominate ADAS, the autonomy market offers fertile ground for startups producing sizable AI silicon. Yet automotive OEMs are also turning vertical, as exemplified by Tesla’s “Full Self‑Driving” computer and Volkswagen’s announced plans to design high‑power chips.

Arteris receives inquiries from OEMs seeking to understand the entire stack and maintain control over the silicon that will redefine vehicle architecture.

Startups like Recogni, Blaize, and Mythic target automotive as an edge AI segment, though the exact deployment paths remain uncertain.

Krewell notes that automotive platforms are still evolving. Distributed architectures offer modularity and risk mitigation but incur higher cost and complexity. He emphasizes the importance of balancing edge intelligence to reduce data traffic, latency, and power distribution.

AI battle shifts from chips to softwareBoth Moll and Krewell agree that the focus is moving from silicon to software. Deploying ML requires robust software ecosystems and low‑code tools that enable embedded designers to create custom models for specific applications.

When asked why he returned to Arteris, Moll cited two reasons: first, Arteris occupies a critical niche in assembling large, complex SoCs via NoC IP; second, the acquisition of Magillem has added a powerful software layer that complements the hardware offerings.

In conclusion, the AI landscape is evolving. While startups face stiff competition from in‑house hyperscaler solutions, opportunities remain—particularly in edge and automotive markets—provided they innovate in silicon and software integration.

>> This article was originally published on our sister site, EE Times.

Internet of Things Technology

- OpenDDS vs. RTI Connext DDS: Choosing the Right Data Distribution Service Solution

- Rigorous Software Testing at RTI: Ensuring Reliability Across Connext DDS

- Achieving ISO 26262 Certification for Automotive Software Components

- The Story & Science of Potato Chips: From George Crum to Modern Production

- Over‑the‑Air Software Updates in IoT: Why SOTA Matters

- Startups Pioneer Battery‑Free IoT with Energy Harvesting

- GE Launches $1.2B IIoT Spin‑Off to Strengthen Digital Portfolio

- The Rise of IoT: Why Security Must Be Built In from Day One

- Tata Expands Reach in Industrial Internet of Things

- Efficient ISD1700 Audio Recording Software & Arduino Setup Guide